As oil traders brace for the opening of markets on Monday, March 2, 2026, the escalating conflict between the United States, Israel, and Iran is shattering the prevailing narrative of an oil glut. For months, analysts have pointed to oversupply concerns, with Brent crude averaging around $63.85 per barrel in forecasts just days ago.

But the recent strikes on Iran, retaliatory actions, and disruptions in the Persian Gulf have injected a massive risk premium into prices, highlighting how fragile global energy markets truly are. Over-the-counter trading already shows Brent jumping 10% to about $80 a barrel, and experts warn of further spikes if tensions persist.

The Incidents Fueling Market Turmoil

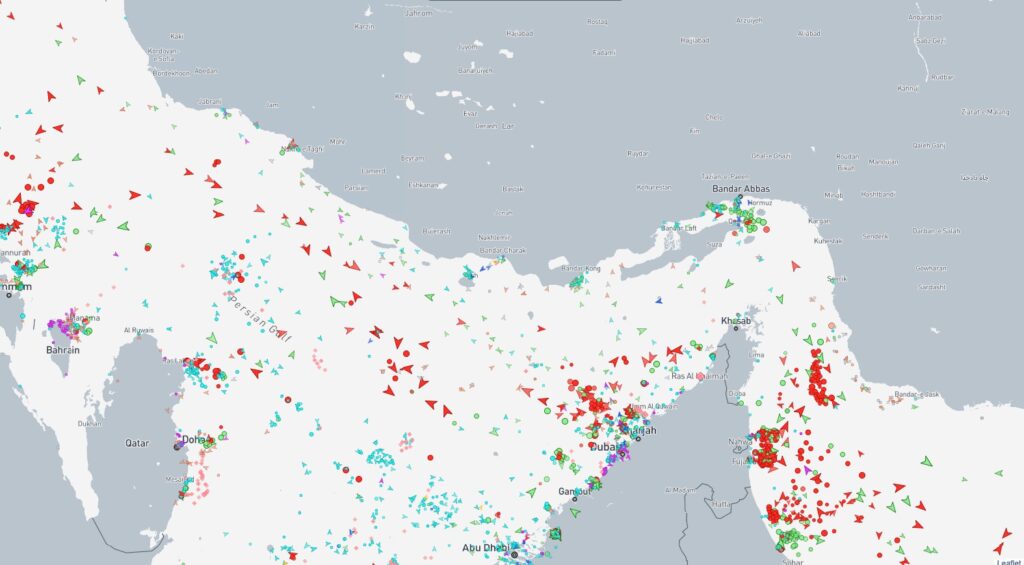

The conflict took a bizarre turn when Iranian forces reportedly attacked one of their own “shadow fleet” tankers, the Palau-flagged Skylight, off Oman’s Musandam peninsula.

This vessel, carrying Iranian oil under U.S. and EU sanctions, was struck near the Strait of Hormuz, injuring four crew members—mostly Indian nationals—and forcing a full evacuation.

The attack marks the first incident near Oman amid the broader U.S.-Israeli strikes on Iran, which have drawn the region into open warfare.

At least three tankers have been damaged in the Gulf, with shipping sources attributing the risks to collateral damage from Iranian retaliation.

While Iran has stated it does not intend to fully shut the Strait of Hormuz—a vital chokepoint for 20-30% of global oil and gas supplies—the waterway’s traffic has ground to a near halt.

Vessels are receiving radio warnings from Iran’s Revolutionary Guards to avoid transit, leading to hundreds of ships dropping anchor.

The slowdown isn’t primarily due to military blockades but skyrocketing insurance rates. War risk premiums for Gulf transits, previously around 0.25% of a ship’s value, are expected to surge 25-50% when underwriters reassess on Monday.

Insurers have already begun canceling policies, forcing oil majors like Chevron and trading houses to suspend shipments.

This has left over 200 commercial vessels idling, tightening vessel supply and pushing freight rates to multi-year highs.

Oil Price Predictions: A Volatile Reopen Ahead

Traders are positioning for a sharp upward gap when markets reopen. Prediction markets like Polymarket show a 95% chance of WTI crude rising on March 2, with odds favoring prices above $80 by month’s end.

Analysts estimate an initial $8-10 per barrel jump, potentially escalating to $10-20 if de-escalation fails or the Strait remains disrupted.

In a prolonged Hormuz crisis, prices could hit triple digits—$100-120 for Brent—evoking a 1970s-style energy shock.

RBC’s Helima Croft notes Middle East leaders have warned of $100+ oil if the war expands.

OPEC+ is responding by planning a larger-than-expected output hike of up to 548,000 barrels per day (bpd) in April, with Saudi Arabia and the UAE already ramping exports.

This could mitigate some losses, but a full Strait closure might remove 8-10 million bpd from markets, even after rerouting via pipelines.

WTI has already surged 22% from December lows to $67.78, its highest since August 2025.

Social media buzz on X reflects trader anxiety, with posts warning of $80-100+ spikes and calls to monitor tanker insurance premiums.

Regime Change Scenario: Lessons from Venezuela

Speculation abounds about internal upheaval in Iran following reports of Supreme Leader Ayatollah Ali Khamenei’s possible death.

If the Iranian people seize control, the U.S. might impose sanctions similar to those on Venezuela, targeting oil revenues to curb regime activities. In Venezuela, U.S. sanctions since 2017 slashed oil production from over 2.5 million bpd to around 1 million bpd, crippling exports and fueling a humanitarian crisis with hyperinflation, food shortages, and millions fleeing as refugees.

The measures froze assets, blocked PdVSA transactions, and imposed tariffs on importers, reducing government revenue by billions.

The United States imposed controls on Qatar, and Secretary Bessent is expected to deliver $5 billion to Venezuela this year. When you look at the deep discounts Venezuela was offering on oil to China, and not getting money, but goods and services marked up by China, the Venezuelans stand to make a lot more money.

The monetary system imposed by the United States through Qatar could eliminate funding for the Houthis, and other proxy fighters, and allow money be used for the Iranian people. This is Crucial, and it also breaks the current global monetary controls over the oil markets. That global control has been in place since BP was created, and the real loser is the Bank of London and the UK. It is not surprising that the UK would not allow the US to use our bases in the UK to launch attacks. We are dismantling their monetary system.

While devastating short-term—exacerbating poverty and mortality—these controls starved Maduro’s regime of funds for corruption and patronage, ultimately contributing to his ouster.

For Iran, similar sanctions could redirect oil revenues away from proxy wars in Yemen, Syria, and Lebanon, channeling more toward domestic trade, food security, and resources for citizens.

A “rapid regime fracture” scenario has 15% odds on some models, potentially normalizing oil flows within 60 days and easing prices.

However, the transition could initially deepen economic woes, as seen in Venezuela’s 80% GDP loss.

Monday Morning Outlook: What Investors and Consumers Should Watch

Markets are on edge for Monday’s open, with WTI potentially gapping to $75-80 and Brent testing $90 if disruptions linger.

A base case of managed escalation (55-60% probability) sees prices peaking then reverting to $75-80 by May.

But a Hormuz crisis (25-30% odds) could shave 1.2% off global growth.

Investors should monitor:

Strait status: Real-time tanker tracking and radio warnings for signs of reopening.

Insurance rates: Surges could prolong avoidance, tightening supply.

OPEC+ actions: Output hikes to offset losses.

De-escalation signals: Diplomatic backchannels or ceasefires.

Geopolitical updates: Further strikes or regime instability.

Consumers face higher pump prices globally. U.S. averages could exceed $3/gallon if crude tops $90, with broader inflation risks.

California’s Vulnerability: Highest Impact in the U.S.?

California, with its high gas taxes and environmental regulations, is poised for the steepest price hikes. The state imports about 60% of its crude, primarily from Alaska, Canada, and Latin America, but global benchmarks dictate local refining costs.

Recent refinery closures, like Valero’s early shutdown, have already reduced supplies, increasing reliance on imports vulnerable to international disruptions.

A $10-20 crude spike could push California averages—already above $4/gallon—higher than anywhere else in the U.S., exacerbating economic pressures amid the conflict.

In summary, the Iran conflict underscores that geopolitical risks can swiftly erase any perceived glut. As Stuart Turley of Energy News Beat often highlights, energy security is paramount—traders, investors, and consumers must stay vigilant in these uncertain times.

Sources: reuters.com, nypost.com, theguardian.com, energypolicy.columbia.edu

Get your CEO on the #1 Energy Podcast in the United States: https://sandstonegroup.us/media/

Is oil and gas right for your portfolio? https://sandstonegroup.us/invest-in-oil-and-gas/

The post The Iran Conflict Exposes the Missing Oil Glut Narrative appeared first on Energy News Beat.