Energy Security Starts at home, and Jason hits Energy Dominance through Service out of the park.

You have heard me say, “Energy Security starts at home, and Energy Dominance comes through your exports”. Well, Jason is a great example of how Energy Dominance can’t happen without exporting our great oilfield services to countries that need to get stranded gas or the know-how rolling.

1. ARC Energy’s Global Operations

Jason Arsenault discusses his company’s presence across 16-17 countries, specializing in designing, selling, and renting equipment for gas processing and energy production. The company focuses on stranded gas monetization, NGL creation, and power generation from underutilized gas resources, with a diverse portfolio of new, reconditioned, and recycled equipment.

2. Venezuela’s Energy Crisis & Opportunities

A significant portion of the discussion centers on Venezuela’s energy sector challenges, particularly the decline of state-owned PDVSA. Given Jason’s personal connections (his wife is Venezuelan), he explores potential opportunities for ARC Energy to help restore production and stabilize the country’s energy industry, with references to U.S. government involvement through Secretary of Energy Chris Wright.

3. Global Unconventional Oil & Gas Expansion

The transcript covers the growing development of shale and unconventional plays in countries like Turkey, Bahrain, and Saudi Arabia. There’s emphasis on how American service companies and technologies can capitalize on these opportunities by providing specialized skills and equipment needed for unconventional reservoir production.

4. Regulatory & Operational Challenges

A key theme is the contrast between regulatory environments—particularly highlighting the difficulty of obtaining permits in California versus the relative ease in other countries. This underscores the importance of local partnerships and understanding regional regulatory and political landscapes.

5. Natural Gas’s Role in Energy Transition

The discussion emphasizes natural gas as a cleaner energy source, focusing on reducing flaring and methane emissions through capturing and monetizing stranded gas resources while minimizing environmental impact.

Connect with Jason on his LinkedIn: https://www.linkedin.com/in/arcenergyequipment/

Check out ARC Energy: https://www.arcenergy.com/

We covered Venezuela, and here is an update on how that is going on.

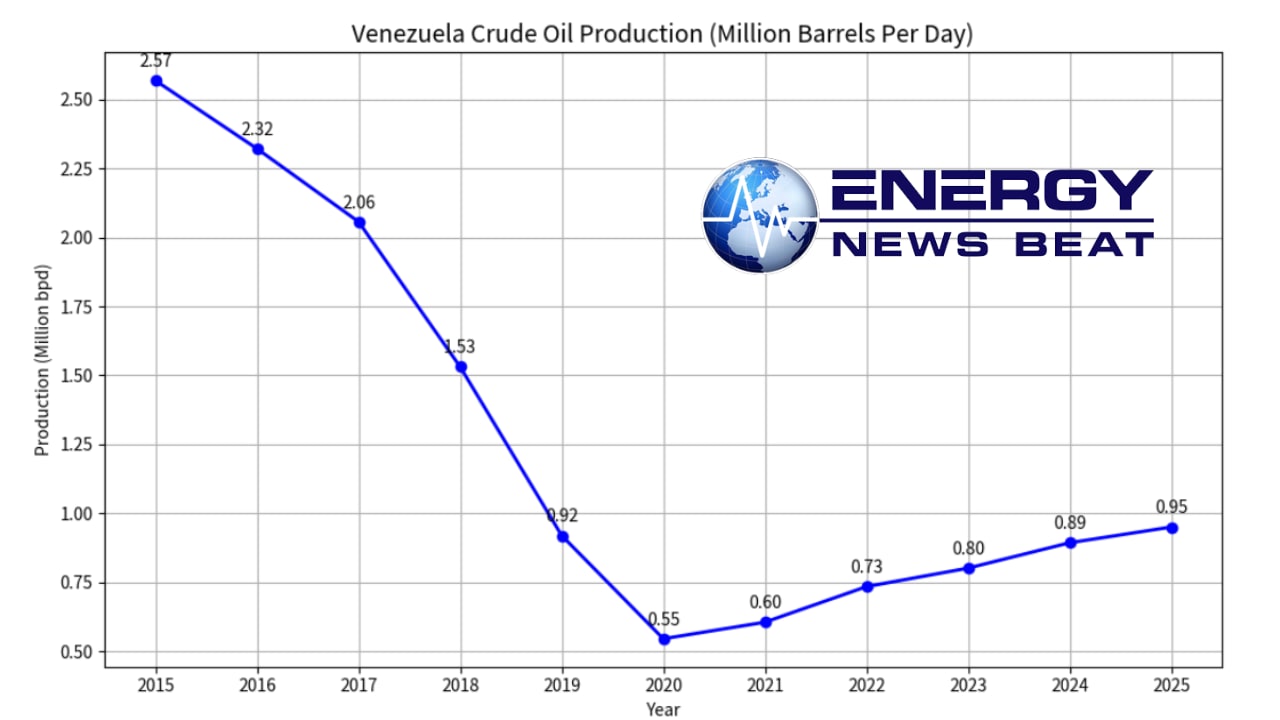

Historical Production Trends

Venezuela’s crude oil production peaked near 3 million barrels per day (bpd) in the late 1990s/early 2000s but has undergone a dramatic decline followed by a modest recovery.

Key annual averages (million bpd, approximate): 2015: 2.57

2016: 2.32

2017: 2.06

2018: 1.53

2019: 0.92

2020: 0.54 (pandemic/sanctions low)

2021: 0.60

2022: 0.73

2023: 0.80

2024: 0.89

2025: ~0.90–1.00 (with monthly peaks near or above 1.0 million)

Production rebounded in 2021–2025 thanks to Iranian technical assistance (diluents and crude swaps), partial U.S. sanctions relief, and joint-venture activity with foreign partners. Early 2026 monthly figures hovered around 900,000–1.02 million bpd before geopolitical developments introduced volatility.

Recent Export Volumes

Exports generally track production (minus domestic refining use, which has been limited by refinery downtime). 2021: ~263,000 bpd (sanctions nadir)

2022: ~442,000 bpd

2023: ~621,000 bpd

2024: ~650,000–800,000 bpd (CEIC data showed 655,743 bpd in Dec 2024)

2025: 750,000–966,000 bpd average, with peaks of 966,000 bpd (August) and sustained levels above 900,000 bpd (November ~921,000 bpd). Tanker data confirmed strong flows throughout the year.

March 2026: Surged to 1.09 million bpd (60 vessels carrying crude, fuel, and byproducts), the highest monthly figure in months, driven by shipments to India and trading-house activity.

Exports are loaded primarily at the José Terminal complex. Much of the crude is extra-heavy Orinoco Belt grades (e.g., Merey 16) that require blending with diluents for transport.

Government Revenues and Payments

Venezuela’s central bank reported that oil exports generated $18.2 billion in revenues in 2025, a slight dip from $18.4 billion in 2024.

These figures represent gross proceeds to PDVSA and the state, though net government take is reduced by production costs, debt servicing, discounts, and operational expenses. Heavy crude has historically sold at discounts (recently narrowed to ~$5/bbl below Brent in some markets). A significant portion of shipments to China has historically serviced oil-for-loans deals (China extended ~$50 billion in loans over the past decade, with remaining debt estimated at $10–12 billion). Payments have increasingly involved workarounds such as stablecoins (USDT) and third-country rebranding to evade sanctions.

In 2026, U.S. policy shifts have introduced new mechanisms, with some royalties, taxes, and dividends from joint ventures required to flow through U.S.-controlled accounts before partial repatriation.

Major Customers

China has been the dominant buyer for years, absorbing 60–80% of exports (often 700,000+ bpd in peak 2025 months) via direct or indirect routes (frequently rebranded through Malaysia or Brazil for concealment). The U.S. has been a key destination via Chevron joint ventures (Gulf Coast refineries are ideally suited for Venezuelan heavy crude). Other notable buyers include India (volumes surged in 2025–2026), Cuba (energy lifeline, ~24,000–26,500 bpd), and smaller flows to Europe/Spain.

2025 Snapshot (approximate shares): China: ~75–80%

United States: ~15–23% (Chevron-led)

India, Cuba, Malaysia (transit): remainder

Companies Involved

PDVSA (Petróleos de Venezuela S.A.) and affiliates: The state oil company dominates production and exports (often >50% of export value through its subsidiaries).

Chevron: The primary U.S. operator via joint ventures; produced ~25% of national output in recent years and handled significant export volumes to the U.S. Gulf Coast.

International traders: Vitol and Trafigura have carried large shares of cargoes in recent years.

Other partners: Historical involvement from Eni, Repsol, Chinese NOCs (CNPC, Sinopec), and Rosneft; newer licenses have brought in additional Western firms under regulated terms.

Shipping entities: Maersk and specialized tankers handle logistics; shadow fleets and ship-to-ship transfers are common for sanctioned routes.

Outlook and Context

Venezuela’s oil sector remains highly sensitive to politics, sanctions policy, and foreign investment. While 2025–early 2026 showed rebounding volumes and revenues, infrastructure bottlenecks, diluent needs, and geopolitical headwinds continue to cap upside. With the world’s largest reserves, the potential for higher sustainable output exists if investment and stability return — but realizing even 2–3 million bpd would require massive capital and expertise.

Again, thanks to Jason and his team at Arc Energy. I am looking forward to visiting with him again, as he is running around the world providing Energy Dominance as a Service.

A shout out to our great Sponsors:

Check out The Energy News Beat Substack

Also, a shout-out to our great Sponsors:

A shout-out to Steve Reese and the Reese Energy Consulting group for sponsoring the Podcast https://reeseenergyconsulting.com/.

A shout-out to our New Sponsor, Data2 – We will be running an AI Centered Series and have lots of data rolling out!. https://www.data2.ai/resources/the-decision-lag-report

And we have WellDatabase rolling in as a new sponsor.

The post Natural Gas Powering the Future appeared first on Energy News Beat.