On the Energy News Beat Stand Up, we are covering 9 big stories, and they all have a huge impact on the markets, consumers, and investors.

Goldman Sachs validated what we had been writing about, and we also brought up the other downstream products that look to be approaching a critical supply chain breaking point. In California, that is about 3 weeks, and in the EU, it is sooner. They use a lot more imported jet fuel and diesel.

This is going to be a huge week. We have California State Assemblyman Stan Ellis, Mike Ariza, and David Blackmon covering the pending crisis in California on Thursday. Monday is the Energy Realities with Tammy Nemeth, Irina Slav, and David Blackmon, and Tuesday is Tim Stewart, President of the U.S. Oil & Gas Association.

1. Oil and Energy Market Outlook

The discussion centers on Goldman Sachs’ “higher for longer” forecast, suggesting sustained elevated prices for oil, gas, diesel, jet fuel, and gasoline. A key concern is the supply shock in the global petrochemical feedstock market caused by disruptions in the Strait of Hormuz, which could trigger demand destruction and potentially lead to a global recession.

2. US Energy Exports

The podcast highlights record-high US exports of crude oil, refined petroleum products, and petrochemical materials. There’s emphasis on the strategic importance of “energy dominance” and energy security through maintaining strong export capabilities.

3. California’s Energy Crisis

A significant portion addresses California’s energy challenges, specifically:

- Refinery closures are reducing local production capacity

- Growing reliance on imports is driving up fuel prices

- Calls for federal intervention to resolve the situation

4. Geothermal Energy Development

The discussion explores geothermal energy as a potential solution, with estimates of 150 GW of untapped geothermal capacity in the US. However, regulatory barriers and the need for government support are identified as key obstacles to development.

5. Energy Sector Investment Analysis

The podcast includes technical and fundamental analysis of energy stocks, examining companies like Crescent Energy and Baker Hughes, along with stock valuations and investment opportunities in the energy sector.

1.Goldman Sachs: ‘Higher for Longer’ Is the New Reality

This article was a validation from David Blackmon’s Substack that they were validating both of our articles and opinions. But I took it one step further on gasoline, diesel, and other petroleum products.

2.The Global PetroChemical Feedstocks Shock is Unfolding

This is the largest supply shock ever experienced in energy markets—no historical parallel matches the scale or duration of this physical disruption.

Impacts on Key Industries

Agriculture & Food Security

The Sulfur Acid-to-Fertilizer Shock and the Naphtha/BTC Agrochemical Shock are devastating. The Gulf supplies ~20-33% of global seaborne fertilizers (urea up to 46% of trade). Sulfur shortages cripple sulfuric acid production, essential for phosphate fertilizers and copper mining. Nitrogen fertilizers (ammonia/urea) rely on natural gas/LNG feedstock now stranded.

With Super El Niño amplifying weather stress on crops, global food prices are rising fast: wheat +4.2%, fruits/vegetables +5.2%, with worst-case spikes in vulnerable nations (Zambia +31%, Sri Lanka +15%, Pakistan +11%). Farmers in India (mid-July paddy window), Brazil, and China face skyrocketing input costs, threatening yields and profitability.

Petrochemicals, Plastics & Manufacturing

Naphtha and LPG feedstocks for ethylene, propylene, and plastics are in short supply. Asian crackers (Japan ~42% naphtha from ME, South Korea cutting runs by up to 50%) are shutting or slowing. Plastics, packaging, textiles, coatings, and resins—all derived from these—face shortages and price spikes. Downstream hits autos, electronics, pharma, and consumer goods.

Financial Markets & Broader Economy

Oil prices have surged (Brent well above $100/bbl at peaks), driving inflation. Central banks (Fed, RBA) risk amplifying the crisis by tightening policy against supply-driven inflation (Federal Reserve Amplification and RBA Framework in Tindale’s slides). Global GDP growth faces 0.2–1.3% hits depending on duration; recession risks are elevated. Stock markets have sold off; bond yields spiked. Tindale’s PolyCRISIS and Tindale’s Trap warn of de-industrialization in import-dependent economies like Australia.

Other sectors (aviation, shipping, metals) face higher fuel, freight, and input costs.

Regions Hurt the Most—and By What Products

Asia (Hardest Hit Overall): China, India, Japan, South Korea, Taiwan, and Southeast Asia rely heavily on Gulf naphtha/LPG (~35-64% of key fertilizer/chemical imports). India (18% of urea imports), China (methanol/MEG buyer), and East Asia (petchem plants curtailing) face dual energy + feedstock shocks. Food inflation compounds existing vulnerabilities.

Global South / Developing Economies: Africa (Zambia), South Asia (Pakistan, Sri Lanka), and Latin America (Brazil) suffer acute fertilizer-driven food price spikes and reduced agricultural output.

Europe: Secondary but significant hits to energy, fertilizers, and supply chains; higher costs feed into manufacturing and households.

Australia: Tindale’s focus—material supply shock drains capital, erodes productive capacity, and accelerates de-industrialization (Tindale’s Trap).

U.S./Americas: Higher fertilizer and plastic costs hit farmers and consumers, though domestic energy production offers some buffer.

3.Demand Destruction is on the Horizon with a Billion-Barrel Hormuz Oil Shock About to Send Prices Up

When oil is traded on paper for futures, it eventually matches physical delivery prices. Well, we have had the worst supply disruption in the history of the world, and it is about to have a horrible financial crash when it hits. Oil should be around $140, but when it heads that way, it will be like a rubber band.

Have you ever shot a rubber band into the air? It comes back to earth, but the more you pull, the higher it goes, and that is where we are right now.

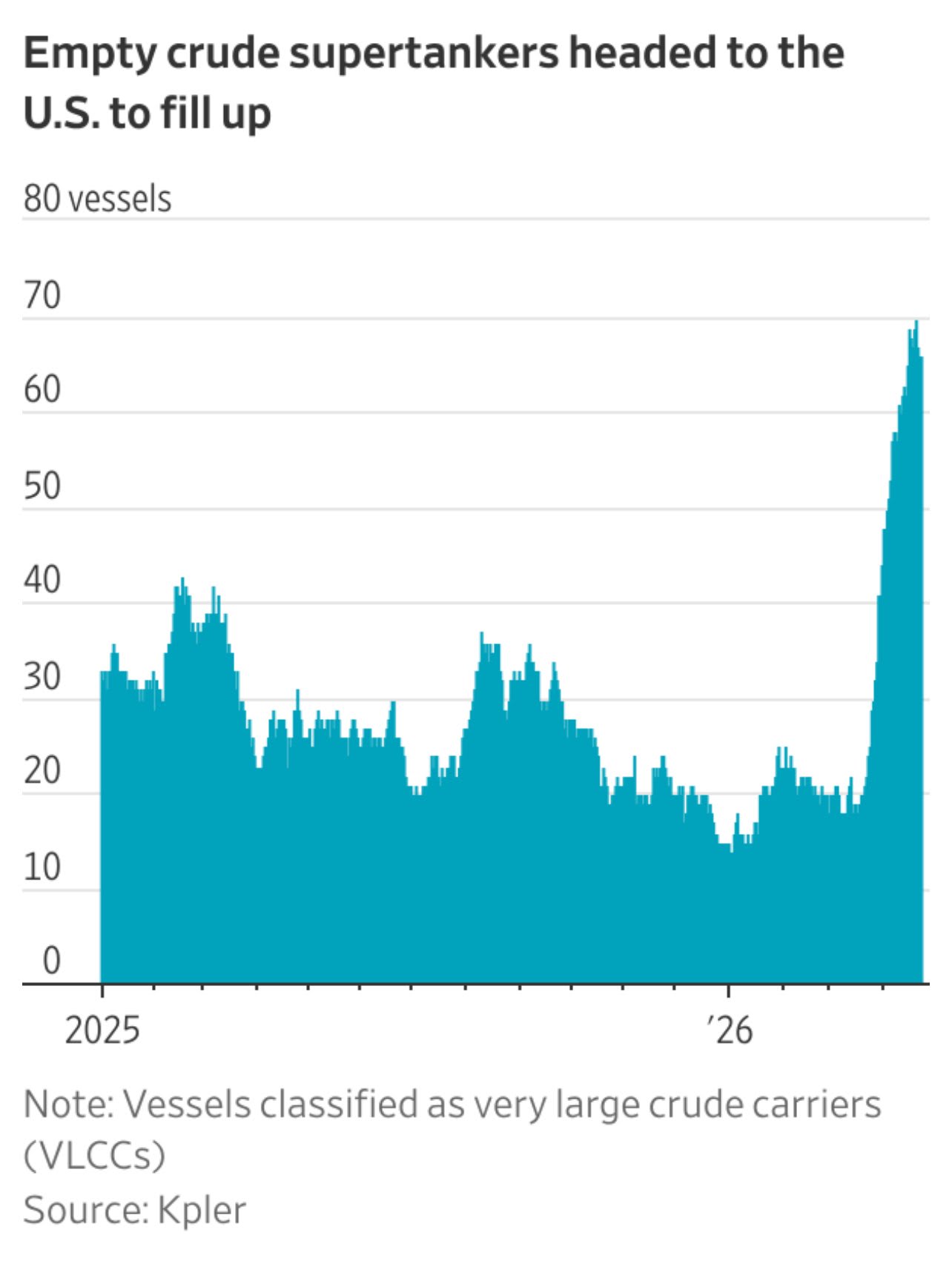

4.US Energy Exports Hit Records as Energy Markets Shift

Record-Breaking Crude and Petroleum Product Exports in 2026 YTD

Year-to-date 2026 data shows a sharp acceleration in U.S. exports compared to 2025 levels. In January 2026, total crude oil and petroleum products exports averaged 10.78 million bpd, building on strong 2025 monthly averages of 10.5–11.4 million bpd (with a December 2025 peak of 11.422 million bpd).

Crude oil exports specifically started the year at 3.922 million bpd in January but have exploded higher. Commodity analysts at Kpler project April 2026 crude exports at a record 5.44 million bpd, with May climbing further to 5.48 million bpd. Weekly data from the U.S. Energy Information Administration (EIA) confirms total crude-plus-products exports hit 12.7–12.9 million bpd in mid-April—the highest on record.

Refined petroleum product exports are also setting new benchmarks. Maritime exports of clean petroleum products (gasoline, diesel, LPG, jet fuel) on clean tankers averaged 6.3 million bpd in January 2026—up about 10% from January 2025 and near record highs, per Vortexa Analytics data cited by the EIA. Total petroleum product exports reached 7.0 million bpd in January (+8% year-over-year). Growth was led by diesel (+19%), gasoline (+7%), LPG (+7%), and jet fuel (+78%).

By March, clean product exports hit a Kpler record of about 3.11 million bpd, with April projections at 3.59 million bpd.

5.U.S. Gasoline Remains a Bargain Compared to Europe – and California

Like the rubber-band point, California will snap up in several weeks for jet fuel, diesel, and gasoline, as tankers are no longer being loaded. They are on the water, and if the government does not make plans now, it will be a real disaster. That will be interesting on Thursday to visit with Assemblyman Stan Ellis.

We don’t have time – here are the steps.

1: Buy tankers

2: Wave the Jones Act and flag them permanently as US Assets

3: Permanently shut the Jones Act down

4: Get our shipyards working

Our congress is incapable of getting voter ID fixed; how can we expect them to do something like fix our shipyards?

This is a great breakthrough, and I have reached out to Tim Latimer, CEO and Co-Founder of Fervo, for an interview on the Energy News Beat Podcast, and we will keep you posted.

Both of the following were good on Earnings.

8.Crescent Energy (CRGY) Valuation Post Earnings and Expectations

9.Baker Hughes Q1 Revenue Beats Estimates by $260 Million as LNG Order Surge

Thank you to all of our great subscribers, patrons, and sponsors. We appreciate you all! Stay safe, pray for our President, Country, and leaders.

A shout-out to Steve Reese and the Reese Energy Consulting group for sponsoring the Podcast

https://reeseenergyconsulting.com/.

Huge opportunity for oil and gas exploration or oilfield service companies to do more with less. Data2: If you have any business systems, can you trust A? Well, they have the patent on validation. https://data2.zoholandingpage.com/energy

And we have WellDatabase rolling in as a new sponsor. https://welldatabase.com/

The post Goldman Sachs says Higher for Longer Is the New Reality – We add that it’s not just oil – it is gas, diesel, jet fuel and everything else. appeared first on Energy News Beat.