Global energy markets have enjoyed an uneasy calm in recent weeks despite the ongoing conflict in Iran and the closure of the Strait of Hormuz. Brent crude has traded in a relatively contained range around $95–110 per barrel rather than exploding past $150 as many initially feared. The reason? China has dramatically slashed its crude and LNG imports, drawing down massive domestic stockpiles to buffer the supply shock. But this strategy is temporary and unsustainable. Analysts warn that Beijing’s imminent return to the market to rebuild inventories could trigger the next major energy price shock—potentially pushing Brent toward $120–130 per barrel or higher in the coming months, especially if the Strait of Hormuz remains closed.

A Supply Deficit, Not a Demand Destruction Crisis

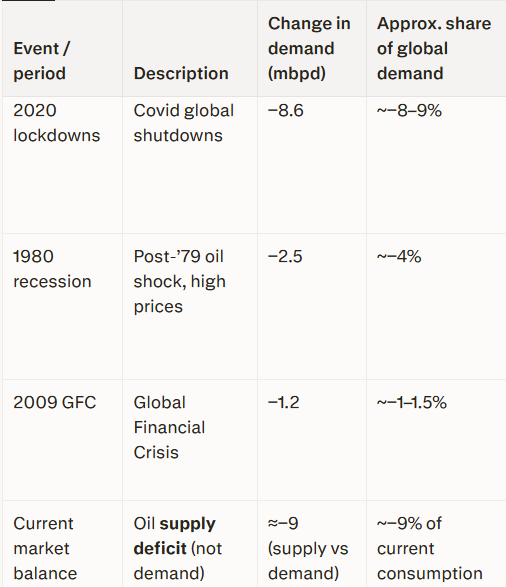

The current situation stands in stark contrast to previous episodes of major oil demand destruction. As highlighted in a recent analysis by energy commentator Lukas Ekwueme (@ekwufinance), the biggest historical demand drops were:

2020 COVID lockdowns: –8.6 million barrels per day (mbpd)

1980 recession (following the second oil shock): –2.5 mbpd

2009 Global Financial Crisis: –1.2 mbpd

In each of those cases, prices collapsed. During the 2020 pandemic, West Texas Intermediate (WTI) briefly went negative (–$37/bbl) while Brent plunged to around $9–20 lows. The 2008–2009 GFC saw Brent crash from a 2008 peak near $147 to roughly $36–40. The 1980 recession followed sky-high prices from the Iran-Iraq war era and led to a later glut and price decline as economies contracted.

Today’s reality is fundamentally different: we are facing a supply deficit of approximately 9 mbpd, not a demand-led collapse. Gulf export capacity has been severely curtailed by the Hormuz disruptions (estimates of 10–14 mbpd lost from the region). Yet prices have not spiked uncontrollably because China has acted as a global stabilizer—cutting imports sharply, running down inventories, and even reselling LNG cargoes. Mobility data remains stable, industrial activity has held up, and there is no broad-based demand destruction. Independent refiners have simply curtailed runs and lived off prior-year stockpiles. This supply-driven tightness has been masked, not resolved.

China’s Inventory Strategy: The Temporary Shock Absorber

According to detailed reporting from OilPrice.com, Chinese crude imports fell to around 6.6 mbpd in May 2026—the lowest level since 2016. April imports were down roughly 20% year-on-year, hitting the lowest since mid-2022. Beijing’s strategic petroleum reserves (estimated at ~1.4 billion barrels) have been aggressively drawn down. On the LNG side, China dramatically reduced spot purchases, resold cargoes to Europe, Japan, and South Korea, and shifted some power generation back to coal—preventing a full-blown bidding war for scarce cargoes.

This approach has kept global inventories from tightening even faster. Goldman Sachs noted that global oil stocks fell by ~246 million barrels in March–April alone and now sit at eight-year lows. The IEA’s April 2026 data similarly underscores the rapid draw. Tanker tracking already shows early signs of normalization—VLCCs carrying Iraqi crude crossing Hormuz under new arrangements, Qatari LNG resuming to China, and even U.S. LNG cargoes returning after more than a year.

But analysts across the board emphasize that this cannot last. China’s mobility indicators are stable, the summer driving season is approaching, and geopolitical risks remain elevated. Rebuilding stockpiles before winter or any further escalation is a national security imperative. Forecasts point to a phased return: an additional 500,000–1 million bpd of crude imports over the next three months (June–August 2026), focused on Russian, Iraqi, and West African grades, alongside selective LNG spot buying and new long-term contracts with the U.S., Canada, and Australia.

What Analysts Are Saying About Oil Prices in the Next Few Months, If the Strait Remains Closed

If the Strait of Hormuz stays closed (or reopening is significantly delayed), the combination of persistent supply losses and China’s stock-rebuild demand surge could rapidly tighten the market further.

The U.S. Energy Information Administration (EIA) currently assumes some reopening and sees Brent averaging around $106 in May/June before easing later in the year. Prolonged closure scenarios push forecasts materially higher.

Firms such as Piper Sandler and Capital Economics have warned of new price highs this summer, with some models projecting $130–140/bbl by late June under sustained inventory depletion.

Goldman Sachs and other major banks have upgraded their outlooks, citing adverse scenarios that could see Brent in the $100–120+ range into Q4, even before factoring in China’s full re-entry.

Consensus among multiple analysts (including those cited in OilPrice.com reporting) is that a China-led demand rebound of 0.5–1 mbpd on top of the existing deficit could drive Brent toward $120–130/bbl quickly, regardless of new escalations.

LNG markets face parallel pressure. China’s return to spot buying and long-term contracting—coupled with Qatar’s Ras Laffan facility damage (removing ~12.8 million tonnes per annum, or 17% of capacity, for 3–5 years)—could reignite the Europe-vs-Asia bidding war and lift Asian and European benchmarks.

Implications and the Road Ahead

The deceptive calm we see today is not equilibrium—it is China temporarily absorbing a massive supply shock. When that absorption ends, the market will feel the full weight of both the ongoing deficit and renewed Chinese demand. Europe and Asia, which benefited from China’s LNG retreat, could face renewed competition and higher prices. Global economic growth, already navigating high energy costs, would face fresh headwinds.

Energy security lessons are clear: opaque national stockpiles can mask tightness for a time, but they cannot replace barrels. Diversification of supply routes, accelerated investment in non-OPEC production, and strategic LNG contracts will be critical.

The next energy shock may not come from a new geopolitical flare-up. It may simply come from China turning the tap back on.

- Original OilPrice.com article: “China’s Return to the Energy Market Could Become the Next Global Price Shock” by Cyril Widdershoven (May 27, 2026)

https://oilprice.com/Energy/Crude-Oil/Chinas-Return-to-the-Energy-Market-Could-Become-the-Next-Global-Price-Shock.html - X post by

@ekwufinance

on major oil demand destruction events and current supply deficit (May 27, 2026)

https://x.com/ekwufinance/status/2059589746557354220 - Supporting analyst and agency references (EIA Short-Term Energy Outlook, Goldman Sachs commodity notes, Piper Sandler and Capital Economics research) as summarized in market reports and the above OilPrice.com analysis. Global inventory data drawn from IEA April 2026 Oil Market Report and Goldman Sachs research cited therein.

- Historical oil price data for demand destruction events drawn from public records (EIA, BP Statistical Review) and cross-referenced in the

@ekwufinance

analysis.

Energy News Beat will continue monitoring tanker flows, Chinese import data releases, and Strait of Hormuz developments for real-time updates.

The post The Next Energy Shock Could Be China’s Return to the Oil and Gas Market appeared first on Energy News Beat.