We cover shipbuilding and even the implications of the Jones Act.

Dr. Beatriz Canamary stopped by the Energy News Beat podcast, and we had a great discussion about energy, exports, and our maritime industry, including shipbuilding and the Jones Act.

I am going to just be brutally honest for a moment, and say that I have been for totally repealing the Jones Act for years. After my discussion with Dr. Canamery, my opinion has shifted toward a more “let’s get the problem solved and leave the Jones Act in place long-term” stance.

But we need a plan to get to a balance. I will have some key Jones Act information below following the video.

Dr. Canamary has a new book coming out, and we will be lining up an interview. Connect with Beatriz on her LinkedIn here: Https://www.linkedin.com/in/beatrizcanamary/

1. U.S. Maritime Industry Revitalization

The core focus is rebuilding America’s shipbuilding capacity. The U.S. currently represents only 0.4% of global ship production (down from over 50% post-WWII), while China dominates with 60% and South Korea adds another 20%. The discussion emphasizes the need for strategic investment in shipyards, workforce development, and predictable cargo demand to justify the expansion of shipbuilding.

2. Energy Security & Dominance Through Maritime

Energy exports (oil and LNG) are central to U.S. dominance, but they’re currently transported on international vessels rather than U.S.-flagged ships. The podcast explores how securing cargo on American vessels strengthens both energy security and the maritime industry. The Strait of Hormuz crisis is cited as a wake-up call about supply chain vulnerabilities.

3. Global Choke Points & Geopolitical Risks

Eight major maritime choke points (Strait of Hormuz, Red Sea/Houthis, Strait of Malacca, etc.) are contested and sometimes weaponized. Insurance companies can effectively shut down shipping by canceling coverage, as Lloyd’s of London did during the Iran strike. The discussion highlights the need for U.S. insurance alternatives and control over critical passages.

4. Nuclear Technology in Maritime

Nuclear propulsion for ships and floating nuclear power plants is presented as an innovation differentiator for the U.S. The ABS (American Bureau of Shipping) has frameworks for approving nuclear projects, and companies like Nano Nuclear are developing micro-reactors designed for maritime use. Nuclear is positioned as cleaner than traditional fuel oil and a competitive advantage.

5. Autonomous & Advanced Maritime Technology

A new IMO (International Maritime Organization) framework for autonomous commercial ships was recently approved, with a mandatory code coming in 2032. The U.S. is positioned to compete through innovation in automation, AI, and autonomous vessels rather than on cost—since labor-intensive competition with China/Korea is unwinnable.

6. Maritime Prosperity Zones

The U.S. should develop regional maritime clusters (similar to Europe’s model) with specialized capabilities—some regions for tankers, others for icebreakers, etc. The American Maritime Industrial Coalition is mapping supply chains and regional expertise to accelerate production.

7. Trade Agreements & Bilateral Partnerships

Strategic trade agreements with U.S. allies can secure cargo flows through American ports on U.S.-flagged vessels, creating demand signals for shipbuilding without direct government subsidies. This creates a win-win for allies seeking energy independence.

8. The Ships for America Act

A bipartisan bill with 126+ seats of support, expected to pass by year-end. It includes tax incentives and supports the broader maritime revitalization strategy outlined in the National Security Strategy and Maritime Action Plan.

9. Geopolitical Shifts & New Trading Blocs

The podcast discusses emerging energy-based trading blocs, China’s port dominance (129 ports globally), and concerns about China’s influence in South America (Peru, Brazil). It also touches on the Monroe Doctrine and regional security in the Western Hemisphere.

10. Ports as Strategic Infrastructure

Dr. Canamari’s forthcoming book explores ports as intelligence hubs, infrastructure assets, and strategic military/trade assets. The discussion covers climate resilience, digital twins, automation, and how ports are increasingly weaponized in global trade wars.

This is a comprehensive discussion of how maritime infrastructure, energy, innovation, and geopolitics intersect to shape U.S. competitiveness and national security.

Dr. Canamary’s key points are really important: the United States has to modernize and automate. Through autonomous loading and ship management, savings can be made. The problem with autonomy is that the labor unions fight it, when they should retrain their unions to embrace it and be part of the path forward. More on that in future podcasts.

The Jones Act—formally Section 27 of the Merchant Marine Act of 1920—requires that all goods transported by water between U.S. ports (including territories like Puerto Rico, Hawaii, and Alaska) must be carried on vessels that are U.S.-built, U.S.-owned, U.S-flagged, and at least 75% U.S.-crewed. Enacted in the aftermath of World War I, it was designed to maintain a strong domestic merchant marine for national security and economic resilience.

Senator Wesley Jones (R-WA) sponsored the legislation, which passed Congress in June 1920 and was signed by President Woodrow Wilson. Its core goal was to ensure the U.S. had a reliable fleet of ships and skilled mariners to support commerce in peacetime and serve as a naval auxiliary in wartime—lessons learned from heavy losses of merchant ships in WWI.

Over a century later, the Jones Act remains a lightning rod. Proponents argue it protects American jobs, shipbuilding capacity, and energy security. Critics say it drives up shipping costs, especially for petroleum products like crude oil, gasoline, diesel, LPG, and LNG, contributing to higher energy prices and forcing regions like California and Puerto Rico to import from foreign sources rather than buy American.

With U.S. energy production at record levels, the law’s limitations are increasingly felt.

From Maritime Powerhouse to Shrinking Fleet: The Numbers Tell the Story

The U.S. once had a robust Jones Act-compliant oceangoing fleet. In 1950, there were 434 such vessels. By 2018, that number had fallen to 99. As of 2025, the large oceangoing Jones Act fleet stands at approximately 93 vessels (31 cargo ships and about 54-56 tankers), with the tankers making up the vast majority of capacity for moving petroleum products.

These ships are older on average than the global fleet, with many general cargo vessels averaging 25-35 years old. Older vessels mean higher operating and maintenance costs, which get passed on to shippers—and ultimately to consumers in the form of elevated fuel and goods prices.

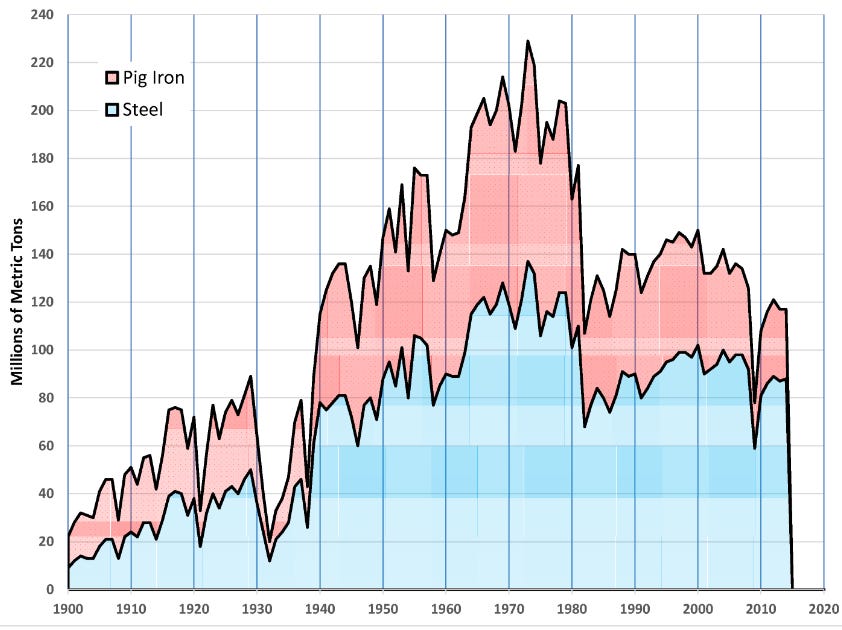

The decline mirrors broader deindustrialization. U.S. shipyards capable of building large oceangoing commercial vessels have shrunk dramatically—from dozens in the mid-20th century to just a handful today. In the 1970s, the U.S. built about 5% of the world’s commercial tonnage (15-25 ships per year). Today, it builds 0.1-0.2%—just 3-5 large vessels annually—while China, South Korea, and Japan dominate.

Steel manufacturing, critical for shipbuilding, followed a similar path. U.S. steel production peaked in the 1970s but has declined amid foreign competition and policy shifts (including reduced subsidies in the 1980s). The U.S. now produces far less steel relative to global output, raising costs for domestic shipyards and making it harder to compete or even build new Jones Act vessels affordably.

Expensive Ships, Expensive Deliveries: The Energy Cost ConnectionJones Act-compliant tankers cost roughly three times more to build than foreign equivalents (e.g., $100-135 million for a medium-range tanker vs. far less abroad). Operating them is also costlier due to U.S. crew wages, regulations, and the age of the fleet. As a result, domestic waterborne shipping of petroleum products can cost 2-4 times more than comparable international routes.

This creates perverse outcomes:

California imports refined products from Asia or routes U.S. Gulf Coast gasoline through the Bahamas (export it first, then import) to bypass Jones Act restrictions—despite abundant domestic supply. California’s specialized CARB-compliant fuels add complexity, but the Jones Act makes intra-U.S. shipping uneconomic.

East Coast and other regions often source fuel from overseas rather than the Gulf Coast, even as the U.S. exports record volumes of energy.

Studies estimate the Jones Act adds hundreds of millions annually in higher energy costs nationwide, with East Coast gasoline, jet fuel, and diesel prices elevated by $0.63–$0.82 per barrel in recent analyses.

Puerto Rico: A Stark Case Study

As a U.S. territory, Puerto Rico falls under the Jones Act. It has no domestic refining capacity and relies heavily on imported petroleum and LNG for power (fossil fuels still dominate its grid). Without Jones Act-compliant LNG tankers (none exist in the fleet), the island has long sourced energy from foreign suppliers like Trinidad & Tobago, driving up costs.

Recent events highlight the bottleneck—and the potential. In 2026, amid global energy disruptions from the Iran conflict, the Trump Administration issued a temporary 60-day Jones Act waiver for energy products. This allowed foreign-flagged vessels to carry U.S. fuel directly to Puerto Rico. In the waiver’s early period, Puerto Rico received over 1.8 million barrels of fuel from the U.S. mainland—shipments that far exceeded typical Jones Act volumes in recent decades and demonstrated what unrestricted access to U.S. energy could achieve.

Under strict Jones Act rules, such domestic energy flows have been severely constrained for years due to the lack of suitable vessels. The waiver proved that U.S.-produced energy can reach PR affordably when shipping capacity exists—but the U.S. fleet simply isn’t there right now.

The Path Forward: Keep the Jones Act, But Fix the Capacity Crisis

The Jones Act’s original intent—national security and a viable U.S. merchant marine—remains valid. A strong domestic fleet supports jobs (hundreds of thousands tied to Jones Act operations), protects against foreign supply disruptions, and ensures sealift capability in emergencies. Repealing it outright would further erode U.S. shipbuilding and maritime expertise.

But deindustrialization over the past 60 years has left us with too few, too-old ships. Short-term, this means we cannot efficiently move our own abundant energy to domestic markets like California or Puerto Rico. We are effectively exporting U.S. energy while importing foreign substitutes at higher delivered costs.

The solution is not repeal, but revival:

Short-term: Targeted waivers during crises (as done in 2026) to prevent supply shocks, while prioritizing U.S. energy flows.

Medium to long term: A national plan to rebuild capacity. Congress and the administration should incentivize the construction of new Jones Act tankers and vessels—through targeted subsidies, tax credits, or public-private partnerships. Buy and reflag modern tankers where possible, but prioritize U.S. shipyards to meet the “built in the U.S.” requirement. Revive steel production and related supply chains. Invest in workforce training for shipbuilding and merchant mariners.

Keep the Jones Act’s core protections intact once capacity is restored. This hybrid approach leverages America’s energy strength without sacrificing security.

With U.S. petroleum production booming, the Jones Act should enable—not hinder—American energy dominance. By addressing the manufacturing gap we created over decades of deindustrialization, we can make the law work as intended: cheaper, more reliable domestic energy delivery and a stronger maritime backbone for the 21st century.

Unfortunately, the Unions are needed, but sometimes they actually hinder the process. This is one time the Unions may need to work on how they capture many of the jobs, as we have to modernize to remain competitive. We have lost the American Compdive drive and manufacturing we once had, and we have to find new ways of doing business to restore our great heritage.

I am looking forward to Dr. Canamary’s book coming out and seeing how her plans shake up energy, shipping, and Energy Dominance over the next 100 years.

A shout-out to Steve Reese and the Reese Energy Consulting group for sponsoring the Podcast https://reeseenergyconsulting.com/.

Data2 if you have any business systems, can you trust A? Well, they have the patent on validation. . https://data2.zoholandingpage.com/energy

And we have WellDatabase rolling in as a new sponsor.

The post Maritime Operational & Governance Strategy for Infrastructure Investors with Dr. Beatriz Canamary – Huge Impacts in Energy appeared first on Energy News Beat.