Special Guest David Blackmon on the Energy News Beat Stand Up.

What a day on the EnergyNews Beat News Desk, we have 10 big stories for you, and as we were filming this, President Trump calls off the plans – wow, changed everything. David Blackmon’s Energy Additions Stops by the Energy News Beat Stand Up as we used one of his stories on blackmon.substack.com.

Make no mistakes, this war will end in one of two ways. World War III, or the Venezuelan-style controls on Iran, as they have shown themselves to be an untrustworthy neighbor and have murdered tens of thousands of their own citizens.

As David and I were signing on to film the podcast, President Trump called off the strikes to take Kharg Island, and I am hoping this is to reposition assets and give some surprise to their capture. The oil markets dropped to $87. 94 for WTI, and this brings up the Paper trading versus the Physical delivery price of $140.

1. Iran Geopolitical Crisis & Military Strategy

The hosts extensively discuss U.S.-Iran tensions, focusing on President Trump’s shifting positions on military strikes and seizing Cargo Island. They analyze three phases of military action: (1) stabilizing oil prices by moving ships through the Strait of Hormuz, (2) degrading Iran’s military capabilities, and (3) direct action inside Iran. A key point is that without “Venezuelan-style controls” on Iran’s oil exports, hostile actors could profit significantly.

2. Oil Markets & Strategic Petroleum Reserve (SPR)

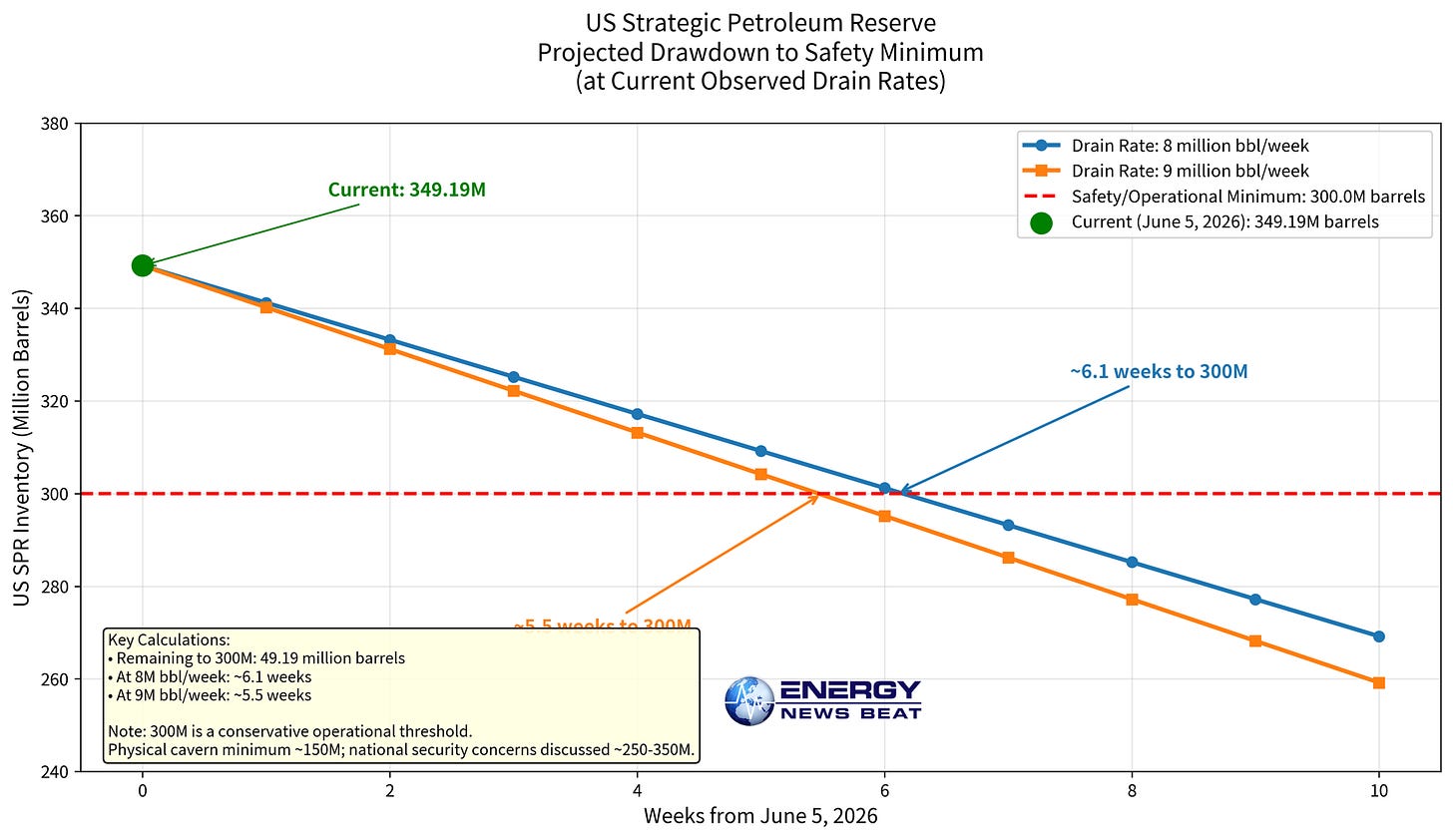

The podcast explores why physical oil prices exceed $140 while futures trade below $100. Key factors include China’s reduced crude imports (4 million barrels/day reduction), alternative export routes bypassing the Strait of Hormuz (7-10 million barrels/day), and tanker truck alternatives. Critically, they warn that the U.S. SPR is dangerously low—only 6.1 weeks away from the safe operational level of 300 million barrels.

3. Global Energy Infrastructure & Pipeline Development

Multiple countries are building alternatives to the Strait of Hormuz to reduce Iran’s leverage. Kuwait is negotiating pipelines with Saudi Arabia and UAE. Japan signed a major LNG deal. This reflects a broader theme: the world is reducing dependence on chokepoints Iran controls.

4. U.S. Energy Policy & Data Centers

Governor Abbott’s directive requires data centers in Texas to fund their own electrical infrastructure, protecting the grid. Texas is becoming the data center capital (second only to Virginia), with massive natural gas reserves in the Permian Basin to support expansion.

5. Natural Gas Pipeline Expansion

Kendra Morgan’s Gulf Express pipeline expansion will come online soon, preventing flaring and enabling 4.5 BCF of new Permian outbound capacity by 2026—a significant development for energy markets.

6. Banking & Investment in Fossil Fuels

The world’s 65 largest banks invested $906 billion in fossil fuels in 2025, with the Iran conflict expected to escalate exploration, production, and energy security spending. The ordering of 250 supertankers signals long-term confidence in oil demand.

7. Political Concerns & Congressional Dysfunction

We express frustration with President Trump’s inconsistent messaging on Iran policy and criticize Congress for its lack of support, calling for primary challenges against most incumbents.

10 Big Stories today.

1.Trump: US Will ‘Assume Total Control’ Of Iran’s Oil Infrastructure

This first story was from Substack and was very cool until 5 min before we started, and then it became stale.

This is incredibly important, and I will go on record and say that we have to gain control of the Iranian oil money, as they have lost the right to control their own destiny.

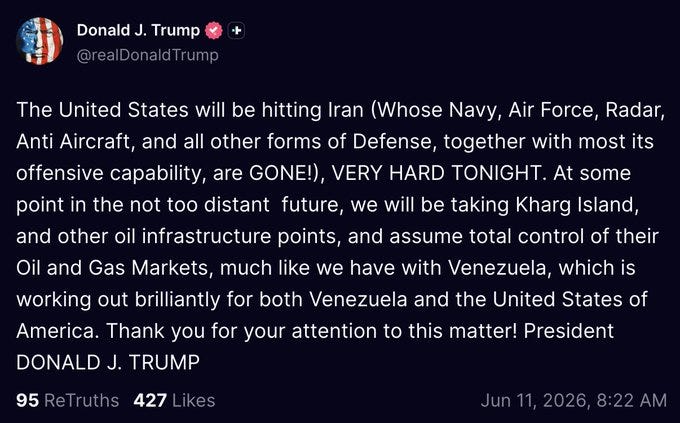

Trump’s Statement on Truth Social and Kharg Island

President Trump posted on Truth Social that the United States will hit Iran hard tonight following recent airstrikes. He further stated that “at some point in the not too distant future, we will be taking Kharg Island and other oil infrastructure points and assume total control of their Oil and Gas Markets.”

Kharg Island is Iran’s primary oil export terminal in the Persian Gulf, handling approximately 90% of the country’s crude oil exports. It has been a repeated target of U.S. strikes on military infrastructure in recent months, while oil facilities have largely been spared so far.

Trump’s language explicitly references the administration’s recent actions in Venezuela, where U.S. forces captured Nicolás Maduro, and the U.S. has taken a leading role in overseeing oil production and revenues. In Venezuela, American companies were positioned to repair infrastructure, and oil sales proceeds were directed under U.S. oversight to benefit both nations.

Venezuelan-Style Controls: Stu Turley’s Analysis on Energy News Beat

Energy News Beat host Stu Turley has repeatedly argued that “Venezuelan-style controls” represent the clearest path to a decisive outcome in the Iran conflict. In recent podcast episodes and Substack analysis, Turley emphasized that without such controls—effectively cutting off the Islamic Revolutionary Guard Corps (IRGC) from oil revenues—Iran will continue funding proxy groups like the Houthis and destabilizing the region.

Turley noted that seizing or controlling Kharg Island and implementing similar oversight mechanisms could starve the regime of funds while potentially allowing for a transition that benefits the Iranian people and stabilizes global energy flows. This approach mirrors the post-Maduro strategy in Venezuela, where oil infrastructure repair and revenue control were central to U.S. objectives.

Why this matters:

Secretary Scott Bessent just posted on X, “Any damage it inflicts on our allies in the Gulf will be paid for with funds extracted from Iranian Accounts.

Market Reaction to Strikes on Iran and Kharg Island Threats

Markets are highly sensitive to developments involving Iranian oil infrastructure and the Strait of Hormuz (through which ~20% of global seaborne oil typically flows). Previous rounds of U.S. strikes on Iranian targets, including military sites on Kharg Island, have triggered sharp moves in energy prices:

Oil prices typically surge on escalation fears due to supply disruption risks. Historical reactions in this conflict have seen Brent crude rise $5–15+ per barrel in short order when strikes intensify or Hormuz/Kharg threats emerge.

As of June 11, 2026, WTI crude futures are trading around $89–91 per barrel, with Brent in the mid-$90s range amid ongoing volatility and a persistent risk premium.

Stocks often react mixed-to-negative on broader risk-off sentiment, while safe-haven assets like gold rise.

Analysts at firms like Barclays and Eurasia Group have warned of potential spikes toward $100+ for Brent if Iranian exports face sustained disruption or if the Strait of Hormuz remains heavily restricted.

A successful U.S. move to control Kharg Island and Iranian oil infrastructure could eventually increase global supply (by redirecting or restarting exports under new management), but the short-term effect is almost certainly higher prices and heightened volatility as markets price in uncertainty.

Broader Implications

President Trump’s strategy combines maximum pressure with the threat of decisive action on Iran’s economic lifeline. By targeting military capabilities tonight and signaling future control of oil assets, the administration aims to force negotiations or regime concessions while preventing further proxy attacks.

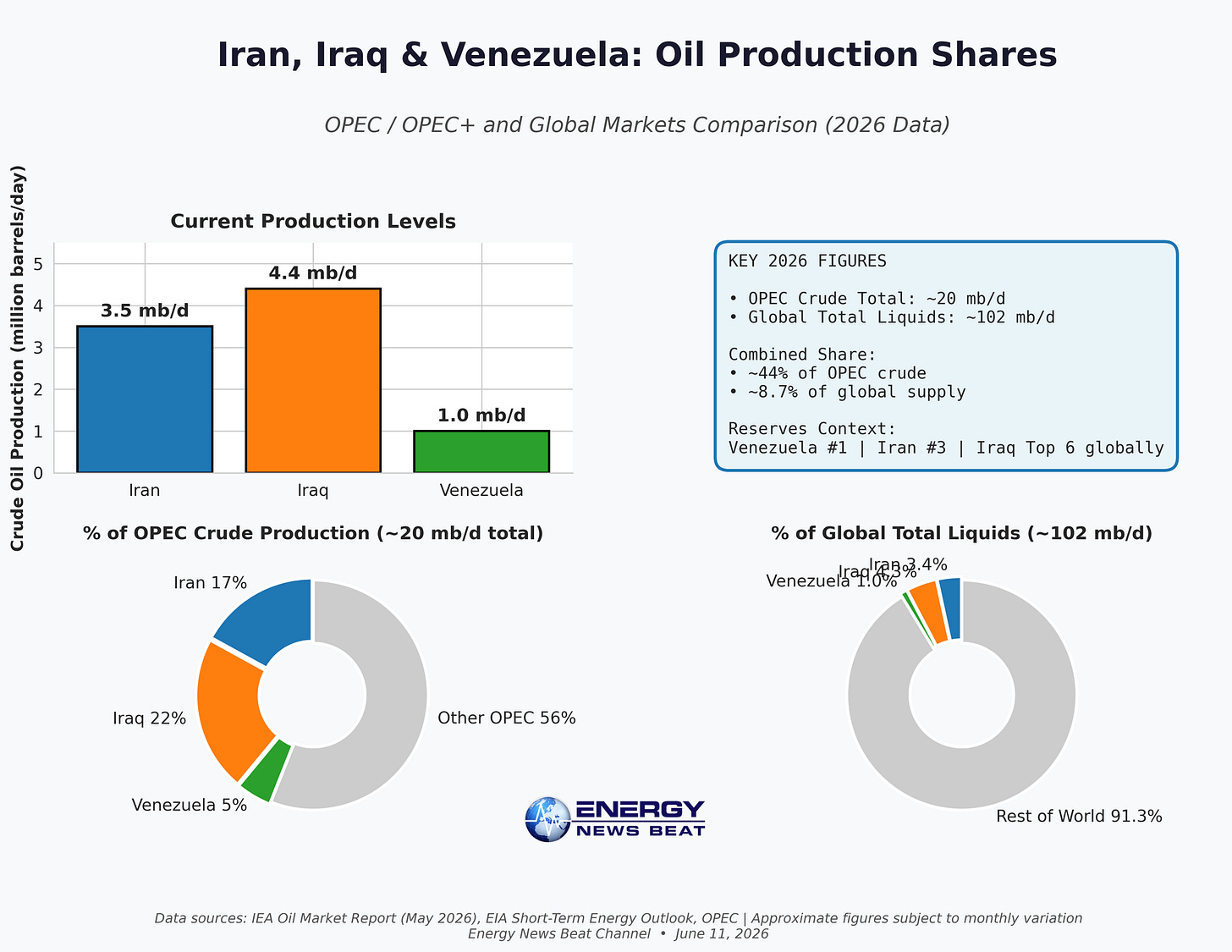

The oil markets just changed again, and let’s not forget that the U.S. still controls the money from Iraq through a different monetary setup, and it would not surprise me if it has shifted toward Venezuelan-style controls to move it away from the Fed. As shown above, the combined oil output from Iran, Iraq, and Venezuela has been about 44% and is now potentially under the United States’ financial controls. One thing to note is that the Iraq system is funneled through the Fed, and it is a privately held organization missing trillions of dollars, and some have indicated it may be a slush fund for foreign countries. The Venezuelan controls implemented by Secretary Scott Bessent appear to be working and helping Venezuela, so this may be a great path forward.

Energy markets remain on edge. Any confirmed move toward “Venezuelan-style” controls on Iranian oil could reshape global supply dynamics, reduce funding for Iran’s proxies, and create new opportunities for Western energy companies—much like the post-conflict plans unfolding in Venezuela. With Secretary Scott Bessent’s comments about the damage caused in the Gulf, I am very hopeful. I would rather pay for damages caused by Iran’s IRGC than allow them to give it to the Houthis or other proxy fighters.

3.Why Oil Is Still Below $100 a Barrel When Physical Oil Is Over $140

4.The Tale of Two SPRs and Different Uses: US and China Navigate the Iran War Supply Shock

The United States is using our SPR to save the world markets, and China is using theirs for China, China, and China.

At the current pace, the SPR could approach or breach commonly cited critical low levels within 5–7 weeks (by mid-to-late July 2026), assuming the release program continues at observed rates. The maximum technical drawdown capability is 4.4 million barrels per day, but actual releases have been more measured.

This drawdown is explicitly intended to supply the global market and ease price pressure amid Middle East disruptions.

China’s Opposite Approach: Living Off Stockpiles

China holds the world’s largest combined strategic and commercial oil inventories—estimated at ~1.3–1.4 billion barrels as of late 2025/early 2026 (government SPR portion ~360 million barrels; commercial/refinery stocks making up the bulk). It added aggressively in 2025 at an average ~1.1 million barrels per day.

In stark contrast to the US:

Sinopec (China’s largest refiner) bought zero Saudi crude for a second straight month.

Saudi July allocations to China: only 12 million barrels (~387,000 barrels per day)—a record low.

Aramco cut its Official Selling Price (OSP) by $ 6 per barrel, yet Chinese buyers largely stayed away because prices remain well above pre-war levels.

China’s May crude imports hit a decade low; refiners are cutting runs at a loss.

China is deliberately drawing down its own stockpiles rather than paying “war premiums.” This buyer strike removes significant demand from the physical market, helping cap rallies. However, these inventories are finite. When Beijing eventually must re-enter the market for secure barrels (recent high-level meetings between China’s energy administration and Aramco officials signal this tension), it could trigger the next leg higher in prices.

Same tool (reserves), opposite strategies: The US floods the global market via SPR releases; China insulates itself by self-supplying from pre-built buffers.

Price Impact and the Paper vs. Physical Disconnect

Despite the most complicated supply disruption mix in history (Iran production risks, Hormuz concerns, broader regional effects), benchmark futures prices have remained relatively contained. As of June 11, 2026, Brent traded around $92/barrel and WTI near $89–91/barrel—far below what many expected given 100+ days of conflict.

Physical markets told a different story earlier in the conflict, with dated Brent and spot grades surging to record premiums (sometimes $30–60+ above futures). By early June, physical premiums had “fizzled out” as refineries recalibrated buying patterns and abating immediate shortfall fears took hold, according to Bloomberg reporting.

However, a notable paper (futures) vs. physical disconnect persists in analyses:Massive crude inventory draws (including SPR and Chinese commercial stocks) are occurring with muted price response.

Traders and observers (including economist Chris Martenson) highlight “wild trades” on the futures tape—e.g., sudden sales of 6 million barrels in a single minute causing price drops with limited follow-through reaction. This has fueled claims of market capture, government-leaning interventions (direct or indirect shorting to manage inflation), or simply overwhelming supply from reserves masking underlying tightness.

The Bloomberg piece notes physical crude grades ripped higher early in the war before easing, with few signs yet of a strong resurgence in premiums.

Who Wins If the Economists Are Right?

If analysts highlighting the unsustainable disconnect (physical tightness masked by reserve draws and possible futures-market dynamics) are correct, the current price suppression is temporary. Key triggers for a sharp re-rating include:

US SPR approaching operational lows (weeks away at current rates).

Chinese stockpiles are running low enough to force a return to the market.

Any escalation or prolonged Hormuz disruption would reduce effective supply further.

Physical delivery realities are catching up as commercial inventories tighten globally.

Potential winners:

Physical crude holders and producers are able to deliver real barrels at higher realized prices.

Those positioned for the eventual re-entry bid from China or a post-SPR exhaustion squeeze.

Long-term bulls who viewed the futures suppression as artificial.

Potential losers:

Consumers and downstream industries are facing a delayed but sharper price spike.

Futures shorts or those betting on prolonged containment.

Policymakers relying on reserve releases as a durable buffer (the SPR is not infinite, and refilling takes time—years at realistic rates).

This is not a simple supply/demand story. It is a high-stakes interplay of government reserve policy, buyer strikes, futures-market dynamics, and finite buffers colliding with real-world supply risks. The “tale of two SPRs” has bought time and moderated prices so far—but the clock is ticking on both the US drawdown and China’s stockpiles.

5.Full Story on the Downed Apache – Part of Getting 22 Tankers through the Gulf

6.Kuwait Oil Chief Seeks Pipeline Alternatives to Skirt Hormuz

7.Japan Inks Major LNG Deal as Energy Markets Focus Away from Hormuz

8.Texas Gov. Abbott Directs PUC and ERCOT to Shield Texans from Data Center and Infrastructure Costs

This is a great thing for Texas, and I have again reached out to John Rich as he was nominated by President Trump as an Agriculture Ambassador to help protect our great American Farms.

A shout-out to Steve Reese and the Reese Energy Consulting group for sponsoring the Podcast https://reeseenergyconsulting.com/.

Data2 if you have any business systems, can you trust A? Well, they have the patent on validation. . https://data2.zoholandingpage.com/energy

And we have WellDatabase rolling in as a new sponsor.

The post We will stop the Bombing When you sign the Deal – or until my next mean Tweet – Energy News Beat Stand Up appeared first on Energy News Beat.